We can't find the internet

Attempting to reconnect

Something went wrong

Hang in there while we get back on track

£313.50

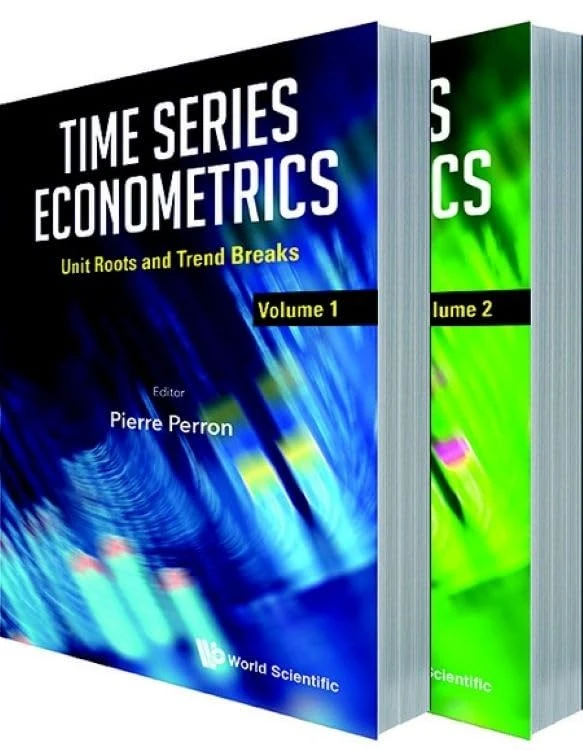

Scientific Publishing Time Series Econometrics (In 2 Volumes)

Price data last checked 38 day(s) ago - refreshing...

We'll watch every seller, every day. One email when your price arrives.

About as cheap as it gets. The only time it was cheaper was 3 months ago.

£314 today · all-time low £304 (Apr 2026) · usually the usual

NEW HERE?

Amazon shows you one price. We show you all of them.

Tosheroon watches Amazon prices so you don't have to. Every product on Amazon has a price history — we make it visible. Set the price you'd actually pay, and we'll email you the second it gets there. No app, no account, one email.

WHAT'S ON THIS PAGE

when this has been cheap or pricey

where the price is heading next

all-time high & low, recent range

name your number, we'll email you

Price History & Forecast

Grey patches = out of stock. Cheaper = lower on the chart. Hover for exact prices.

Last 53 days · 53 data points (no recent data)

Price Distribution

Price distribution over 53 days • 3 price levels

Price Analysis

Most common price: £315 (26 days, 49.1%)

Price range: £304 - £315

Price levels: 3 different prices over 53 days

Description

Product Specifications

- Brand

- Scientific Publishing

- Format

- hardcover

- ASIN

- 9813237856

- Domain

- Amazon UK

- Release Date

- 18 April 2019

- Listed Since

- 08 February 2018

Barcode

No barcode data available

Similar Products You Might Like

Multivariate Time Series Analysis: With R and Financial Applications (Wiley Series in Probability and Statistics)

Wiley

Analysis of Integrated and Cointegrated Time Series with R (Use R!)

Springer

Applied Time Series Analysis and Forecasting with Python (Statistics and Computing)

Springer

Time Series and Dynamic Models (Themes in Modern Econometrics)

Cambridge University Press

Econometric Analysis of Financial and Economic Time Series: Part a: 20, Part A (Advances in Econometrics, 20, Part A)

Jai Press Inc.

Essentials of Time Series for Financial Applications

Academic Press

Advances in Time Series Data Methods in Applied Economic Research: International Conference on Applied Economics (ICOAE) 2018 (Springer Proceedings in Business and Economics)

Springer

Time Series Analysis and Forecasting by Example: 301 (Wiley Series in Probability and Statistics)

Wiley

Financial Risk Management with Bayesian Estimation of GARCH Models: Theory and Applications: 612 (Lecture Notes in Economics and Mathematical Systems, 612)

Springer

Structural Changes in Nonstationary Time Series Econometrics: Time Varying Cointegration and Modeling Catastrophic Events

VDM Verlag

Long-Memory Time Series: Theory and Methods (Wiley Series in Probability and Statistics)

Wiley

A Course in Time Series Analysis: 322 (Wiley Series in Probability and Statistics)

Wiley

Time Series Modelling with Unobserved Components

CRC Press

Linear Time Series with MATLAB and OCTAVE (Statistics and Computing)

Springer

An Introduction to Applied Econometrics: A Time Series Approach

Red Globe Press

The Art and Science of Econometrics (Routledge Studies in Economic Theory, Method and Philosophy)

Routledge

Time Series Analysis: Nonstationary and Noninvertible Distribution Theory: 4 (Wiley Series in Probability and Statistics)

Wiley

Multivariate Modelling of Non-Stationary Economic Time Series (Palgrave Texts in Econometrics)

MACMILLAN