We can't find the internet

Attempting to reconnect

Something went wrong

Hang in there while we get back on track

£154.00

Wolters Kluwer Law & Business General Anti-Avoidance Rules for Major Developing Countries (Series on International Taxation 49)

Price data last checked 48 day(s) ago - refreshing...

We'll watch every seller, every day. One email when your price arrives.

It has never been this cheap. We have no record of a lower price.

£154 today · cheaper than every other day in the last 3 months

NEW HERE?

Amazon shows you one price. We show you all of them.

Tosheroon watches Amazon prices so you don't have to. Every product on Amazon has a price history — we make it visible. Set the price you'd actually pay, and we'll email you the second it gets there. No app, no account, one email.

WHAT'S ON THIS PAGE

when this has been cheap or pricey

where the price is heading next

all-time high & low, recent range

name your number, we'll email you

Price History & Forecast

Grey patches = out of stock. Cheaper = lower on the chart. Hover for exact prices.

Last 43 days · 43 data points (no recent data)

Price Distribution

Price distribution over 43 days • 1 price levels

Price Analysis

Most common price: £154 (43 days, 100.0%)

Price range: £154 - £154

Price levels: 1 different prices over 43 days

Description

Product Specifications

- Format

- hardcover

- ASIN

- 9041158391

- Domain

- Amazon UK

- Release Date

- 27 October 2014

- Listed Since

- 24 October 2014

Barcode

No barcode data available

Similar Products You Might Like

Tax Avoidance and Anti-Avoidance Measures in Major Developing Economies

Bloomsbury Academic

Comparative Tax Law

Wolters Kluwer

Tax Avoidance and the Law: Understanding the UK General Anti-Abuse Rule (Routledge Research in Tax Law)

Routledge

Springer - Regulation of Corporate Tax Avoidance (Ius Gentium 12)

Springer

A Guide to the Anti-Tax Avoidance Directive (Elgar Tax Law and Practice series)

Edward Elgar Publishing

Kluwer Law International - Double Non-taxation and Hybrid Entities

Kluwer Law International

Tax Avoidance and European Law: Redesigning Sovereignty Through Multilateral Regulation (Routledge Research in Tax Law)

Routledge

Wolters Kluwer - Hybrid Financial Instruments Book

Wolters Kluwer

The Routledge Companion to Tax Avoidance Research (Routledge Companions in Business, Management and Marketing)

Routledge

Coordination and Cooperation: Tax Policy in the 21st Century: 81 (Series on International Taxation)

Wolters Kluwer

A Multilateral Tax Treaty: Designing an Instrument to Modernise International Tax Law (Series on International Taxation)

Springer

Legal Interpretation of Tax Law, 2nd Edition (Series on International Taxation)

Wolters Kluwer

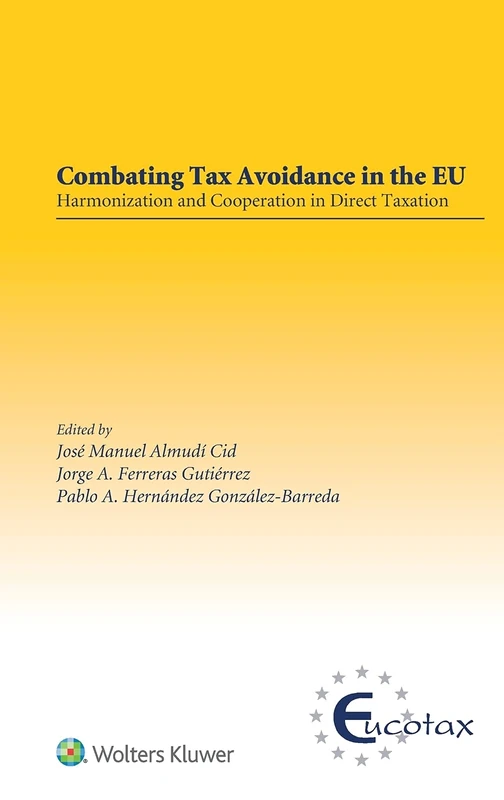

Combating Tax Avoidance in the EU: Harmonization and Cooperation in Direct Taxation (EUCOTAX Series on European Taxation)

Wolters Kluwer

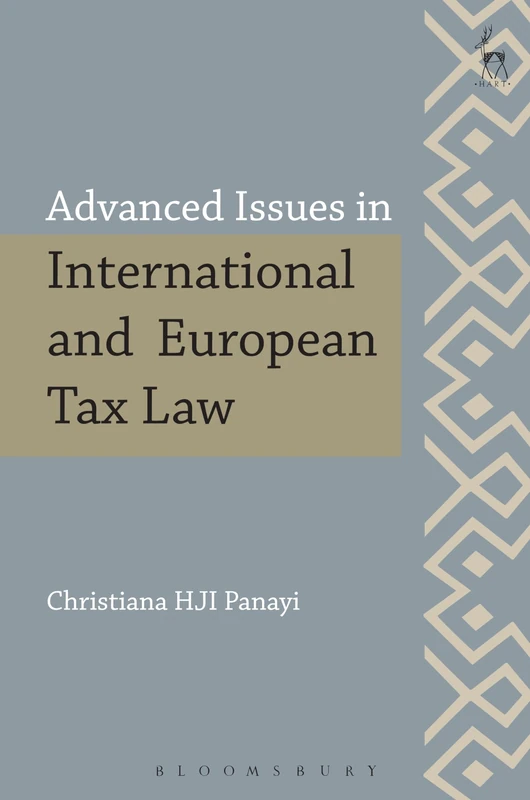

Advanced Issues in International and European Tax Law (Modern Studies in European Law)

Bloomsbury

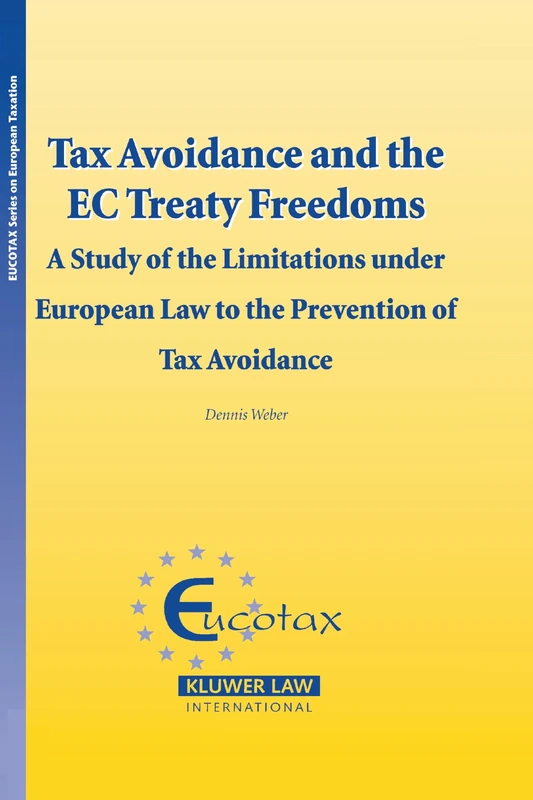

Tax Avoidance and the EC Treaty Freedoms: A Study of the Limitations under European Law to the Prevention of Tax Aviodance: 11 (EUCOTAX Series on European Taxation Series Set)

Kluwer Law International

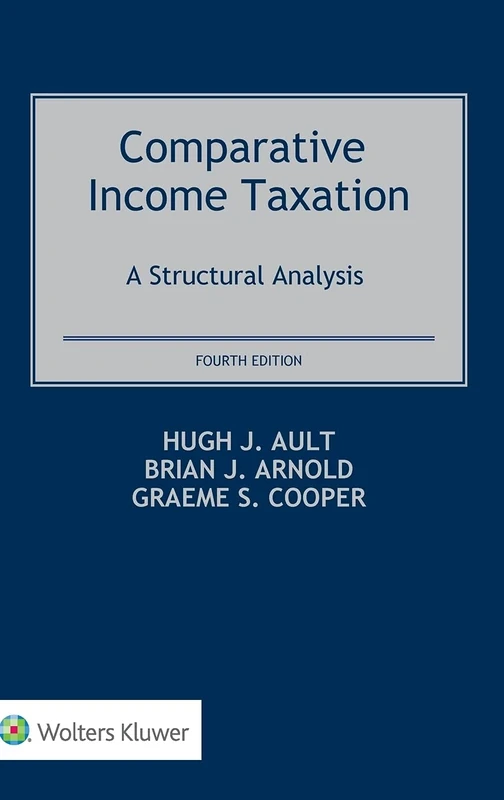

Comparative Income Taxation: A Structural Analysis

Wolters Kluwer

Global Tax Governance: What is Wrong with It and How to Fix It

Parlux

Taxation: Policy and Practice 2018/19 (25th edition)

Company Taxation in the Asia-Pacific Region, India, and Russia

Springer

Taxpayers in International Law: International Minimum Standards for the Protection of Taxpayers' Rights

By

IFA: Abusive Application of International Tax Agreements: Abusive Application of International Tax Agreements (IFA Congress Series Set)

Springer

Taxing Income and Consumption: The Development of International Tax Law and Policy

Edward Elgar Publishing

Bloomsbury Professional - The Regulation of Tax Avoidance Book

Bloomsbury Professional

International Tax Coordination: An Interdisciplinary Perspective on Virtues and Pitfalls: 60 (Routledge International Studies in Money and Banking)

Routledge